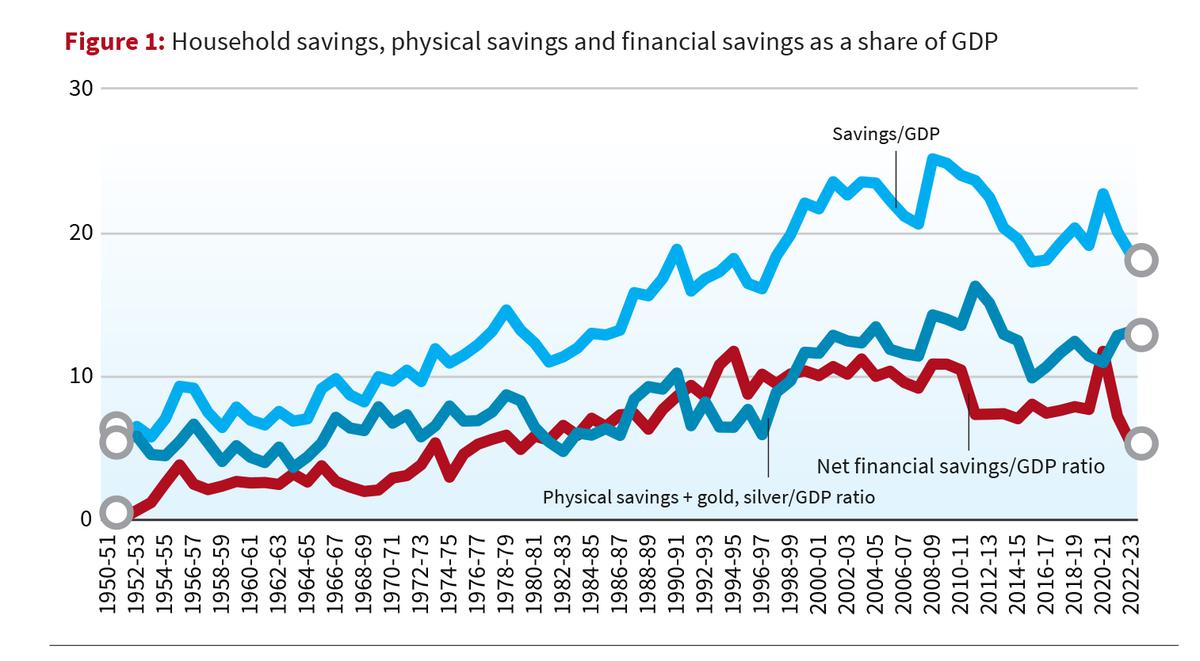

The fall in family financial savings has been on the coronary heart of current debates in India. The decline in family financial savings is led to by a drastic discount in web monetary financial savings because the family web monetary financial savings to GDP ratio attained a four-decade low. Figure 1 reveals the broad development in family financial savings, bodily financial savings and gold, and web monetary financial savings.

The sharp discount in family web monetary financial savings in 2022-23 has been related to an total fall in family financial savings regardless of marginal restoration in bodily financial savings.

Interpreting decrease monetary financial savings

The web monetary financial savings of the family is the distinction between its gross monetary financial savings and borrowing. The gross monetary financial savings of a family is the extent to which its monetary belongings change throughout a interval. The monetary belongings of households sometimes comprise financial institution deposits, forex and monetary investments in mutual funds, pension funds, and so on. Though family borrowing consists of credit score from non-bank monetary firms and housing firms, the majority of the borrowing includes credit score from business banks. In basic, there are no less than three distinct elements that may doubtlessly convey a few discount in family web monetary financial savings.

First, households sometimes finance their further consumption expenditure by rising their borrowing or depleting their gross monetary financial savings. By financing larger consumption expenditure at any given degree of disposable revenue, decrease web monetary financial savings present stimulus for mixture demand and output on this case.

Also learn: No small change: on the elevating of returns on small financial savings schemes

Secondly, when households finance larger tangible (bodily) funding by rising their borrowing or depleting their gross monetary financial savings. The discount in web monetary financial savings on this case stimulates mixture demand and output by means of the funding channel.

Third, when curiosity fee of a family will increase say because of larger rates of interest, households can meet the elevated burden by means of borrowing or by means of depleting gross monetary financial savings thereby inducing a discount in web monetary financial savings.

The first issue hardly performed any position within the sharp discount in gross monetary financial savings in 2022-23 because the consumption to GDP ratio remained largely unchanged between 2021-22 (60.95%) and 2022-23 (60.93%). The second issue performed solely a restricted position. While the gross monetary financial savings to GDP ratio declined by 3 proportion factors (7.3% to five.3%) in 2022-23, family bodily funding to GDP ratio elevated solely by 0.3 proportion level (12.6% to 12.9%) throughout the identical interval. Though larger borrowing is partly financed by curiosity revenue from monetary belongings, it may be largely attributed to larger curiosity funds of the family within the current interval.

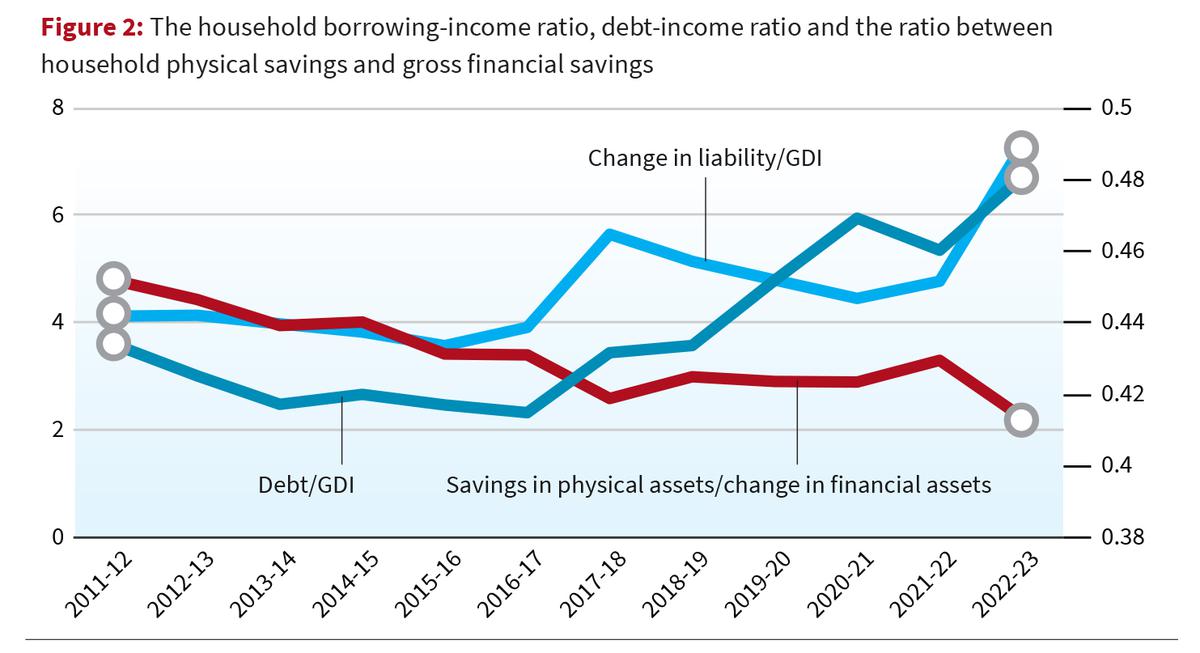

Figure 2 displays this phenomenon by depicting the development in family borrowing to revenue ratio, debt to revenue ratio and the ratio between family bodily financial savings and gross monetary financial savings.

The share of family borrowing in family (disposable) revenue registered a pointy spike in 2022-23. Such an increase in family liabilities was related to a decline within the bodily financial savings to monetary financial savings ratio, indicating a change in family asset composition in favour of economic belongings.

Implication of upper debt burden

The rise in family debt burden has two issues for the macroeconomy.

The first concern is about debt reimbursement and monetary fragility. Since the reimbursement capability will depend on the revenue move, a key criterion for evaluating a family’s debt sustainability is the distinction between rate of interest and the revenue progress price. On the flip aspect, the curiosity funds from the households are the curiosity revenue of the monetary sector. If households fail to fulfill their debt reimbursement commitments, then it reduces the revenue of the monetary sector and deteriorates their stability sheets, which in flip can have a cascading impact on the macroeconomy if the latter responds by decreasing their credit score disbursement to the non-financial sector.

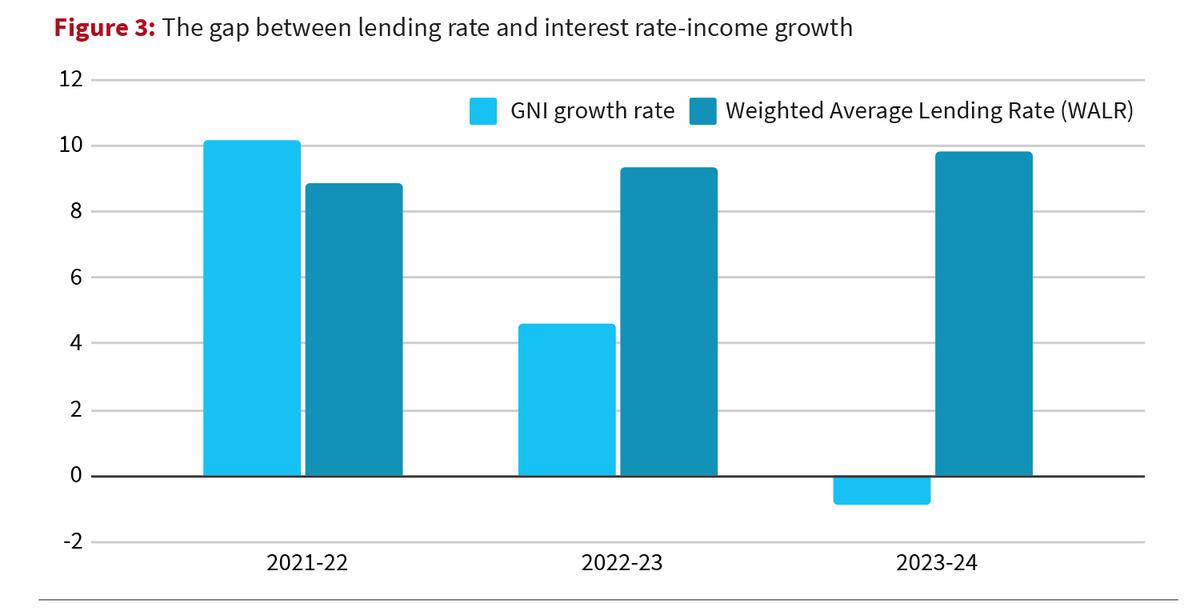

Figure 3 reveals the distinction between the weighted common lending price of scheduled business banks and the expansion price of gross nationwide revenue.

Though the distinction reveals a declining development since 2021-22, the indicator turned out to be damaging within the 2023-24 interval. The sharp discount in rate of interest and revenue progress hole is on account of decrease revenue progress price and better lending price of the business banks. The weighted common lending price registered a pointy rise within the final two years, notably as a result of tight financial coverage stance of the RBI and the sharp rise within the name cash price throughout this era.

The second concern pertains to the implication on consumption demand. Over and above disposable revenue, the consumption expenditure of the family will be affected by their wealth, debt, and rate of interest. Reduction in family wealth can result in decrease consumption expenditure as households might try and protect their wealth place by rising their financial savings.

Higher family debt also can cut back consumption expenditure in no less than two methods. First, if larger family leverage is perceived as an indicator of upper default danger, then it might induce banks to bask in credit score rationing and cut back the credit score disbursement. The consequent discount in credit score disbursement can adversely have an effect on consumption. Second, larger debt can cut back consumption expenditure by rising the curiosity burden, to not point out the impact of upper rates of interest on consumption expenditure.

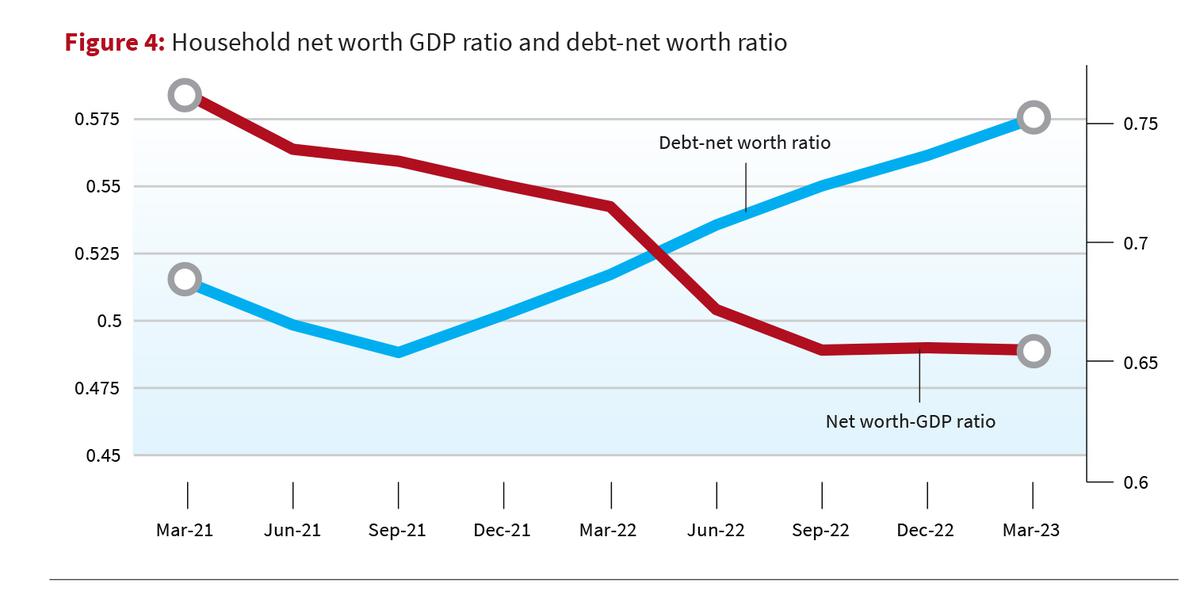

The Indian financial system registered all these tendencies within the current interval. The monetary wealth or the online price of the family is the distinction between the inventory of economic belongings and liabilities. As evident from determine 4, the monetary wealth to GDP ratio of the family has registered a pointy decline within the current interval, together with an increase in leverage of the family as indicated by the rise in debt to web price ratio.

Not surprisingly, the expansion price in non-public ultimate consumption expenditure throughout 2023-24 registered a pointy decline as in comparison with 2022-23.

Macroeconomic implication

The implications of the procyclical leverage by the households together with the compositional change within the asset aspect of the stability sheet, albeit with a fall within the degree of financial savings, for the soundness of financial progress is regarding.

First, on condition that each the move indicator of liabilities to disposable revenue and the inventory indicator of debt to web price reveals an rising development makes the households susceptible.

Second, the coverage mantra of upper rate of interest to counter inflation by decreasing macroeconomic output and employment can depart households with an rising degree of debt of their stability sheets and doubtlessly push the households right into a debt entice. Third, the implications of excessive rate of interest on debt burden can have an hostile influence on the consumption of the households and consequently for mixture demand.

The family stability sheet tendencies point out a broader change within the construction of the financial system. The change in composition of the asset aspect of the family stability sheet in the direction of monetary belongings point out a point of financialisation of the financial system which strikes from a production-based financial system to a financial or monetary exchange-based financial system making the five-trillion-dollar financial system each jobless and fragile.

Zico Dasgupta and Srinivas Raghavendra train economics at Azim Premji University.

Source: www.thehindu.com